Fareed Mohamedi

- Lifting sanctions could revive oil and natural gas production in Iran. Foreign private and national oil companies are looking to invest in the Islamic Republic, particularly in light of changes to investment terms offered by the Iranian government. Plans for pipelines and liquid natural gas could also be revived.

- The Iranian economy is heavily dependent on the lucrative oil and gas sector. The vagaries of oil markets and Iran’s reliance on a single resource for most of its income have created disincentives to develop a more diversified and globally integrated economy. This weakness has made sanctions more potent. But impaired access to imports may have also boosted domestic production to some extent. Nonetheless, the oil and gas sector has been a source of periodic but persistent economic instability.

- Iran’s oil and gas sectors have faced key structural problems. On the demand side, subsidized prices and a population that has doubled since the 1979 revolution have created excessive demand. On the supply side, an aging oil resource base has been stymied by financial constraints, technical shortages, sanctions, and using gas to stimulate oil production.

- One of the ironies of the oil-rich Gulf states’ predicament – Iran’s situation is typical of the region -- is that they are short on hydrocarbon resources. Moreover, as global environmental concerns mount, Gulf countries are facing pressures to curb their greenhouse gas emissions. Both factors are pushing the Gulf to explore alternative energy sources, including nuclear options.

Overview

In 1908, Iran was the first country in the Persian Gulf to discover oil. Petroleum has been the primary industry in Iran since the 1920s. Despite Tehran’s attempts to diversify the economy, the oil and gas industry is still the critical engine of economic growth. Oil revenues over the past few years have accounted for around 60 percent of government revenues. But this figure dropped to 47 percent in 2015 after low oil prices forced the government to revise the state budget. Additionally, oil revenues comprised only around 10 percent of the gross domestic product. This trend has remained fairly steady over the last few decades.

The Iranian government’s dependence on oil revenues has resulted in prolonged patterns of rentierism—or dependence on a single natural resource—in its political economy. Some analysts have claimed that Iran’s “revenue autonomy” and access to large amounts of foreign exchange helped fund an eight-year war with Iraq and extremist groups. But historically, oil attracted external interference by foreign powers, and the sector has suffered in the last several decades. Production was acutely affected during the revolution, especially by workers’ strikes. During the Iran-Iraq War, the invasion of oil-rich Khuzestan and the port of Abadan severely impacted revenues. And Iran’s disputes with Western countries led to sanctions that crippled its ability to buy badly needed equipment and new refineries from the West.

Vulnerabilities

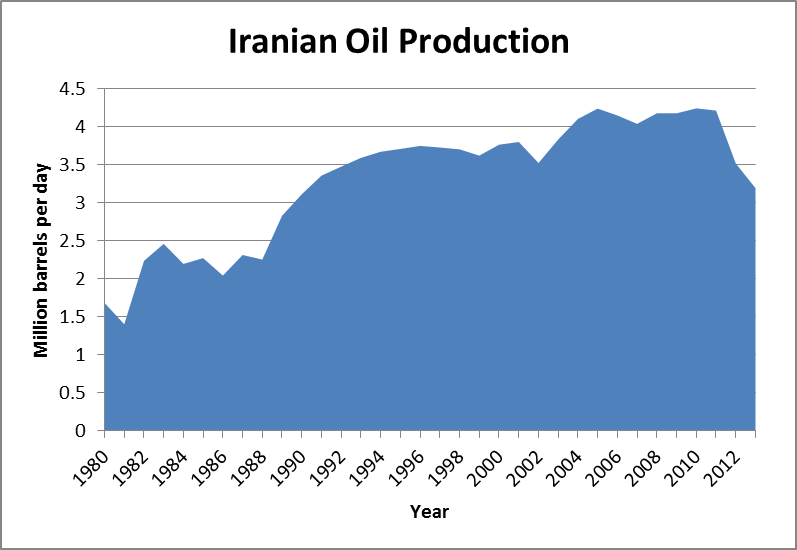

The revolutionary government has struggled since the 1979 revolution to maintain oil production above 3.5 million barrels per day—just over one-half of production under the last shah. Iran produced 6 million barrels per day in the monarchy’s final years. Production fell to a low of 1.5 million barrels per day in 1980. The long period of low oil prices between 1986 and 2000 also crippled Iranian revenues.

Iran’s revenues have fluctuated due to the vagaries of the world’s oil markets, periodically depressing government revenues. The government has often not been able to cut spending for political reasons and funded its deficits by borrowing from the Central Bank. Periodic bouts of lower oil prices have also led to foreign exchange shortfalls and a fall in imports, especially industrial inputs. Excessive domestic demand and disrupted industrial production has led to periods of high inflation.

Misuse of oil revenues has also caused long term-economic problems. After he was first elected in 2005, former president Mahmoud Ahmadinejad embarked on a populist spending program encouraged by higher oil prices. But his plan overcommitted the government to support social welfare, which Tehran could not afford due to sanctions and, later, the drop in oil prices in 2014. Iran had built up its foreign exchange because of higher oil prices over the past decade, but portions of the reserves were impounded by foreign countries as part of the sanctions regime.

When President Hassan Rouhani took office in 2013, he prioritized reforming the oil and gas sector. He appointed Bijan Zanganeh as his oil minister. Zanganeh, who previously held the post under reformist president Mohammad Khatami, claimed that “the problem we are facing now in the petroleum industry is not finance, but management problems.” Zanganeh and Rouhani had some success reforming poor management in the oil industry. But by 2015, international sanctions still restricted the industry from reaching its full potential.

When President Hassan Rouhani took office in 2013, he prioritized reforming the oil and gas sector. He appointed Bijan Zanganeh as his oil minister. Zanganeh, who previously held the post under reformist president Mohammad Khatami, claimed that “the problem we are facing now in the petroleum industry is not finance, but management problems.” Zanganeh and Rouhani had some success reforming poor management in the oil industry. But by 2015, international sanctions still restricted the industry from reaching its full potential. Subsidy Reform

Iran’s longstanding subsidies — to support consumption of refined oil products and natural gas — became a huge burden on the Iranian budget and its balance of payments due to runaway consumption and rising imports of gasoline. Fuel subsidies cost the government $38 billion per year, or around 20 percent of GDP.

The government began an initial phase of subsidy reform in 2010, initiating a second phase in 2014. In May 2015, subsidy cuts raised the price per liter of gasoline from 7,000 rials to 10,000 rials – about $1.28 per gallon.

The International Monetary Fund called the subsidy reform program “unprecedented in Iran’s economic history in terms of its scale, preparations and potential implications.” The government used the higher cash earnings from raising product prices for universal cash transfers to households, direct assistance to public enterprises and budgetary support.

But this move coincided with new sanctions, which led to a deceleration in growth, rise in inflation and currency devaluation. It also led to a sharp fall in cash needed to fund the subsidy removal program. Other inflationary policies by the government undermined the program.

In fact, the government’s efforts did not even reduce refined product consumption. In 2005, Iran consumed 1.3 million barrels per day (bpd) of refined products, 350,000 of which were gasoline. Iran imported around 150,000 bpd of gasoline - nearly 45 percent of consumption. By 2014, demand had growth to 1.6 million bpd, a clear indication that subsidy reform had not been successful in suppressing consumption.

By 2015, Iran had undertaken major efforts to reduce its dependence on foreign imports of refined products. Iran consumed 437,000 bpd of gasoline in 2014, but imports had fallen to a mere 25,000 bpd. Increased refining capacity, even in the face of sanctions, led to near self-sufficiency.

Oil

Iran is the second largest OPEC producer and the fifth largest globally (after Russia, Saudi Arabia, the United States and China). Its oil sector is one of the oldest in the world. Production started in 1908 at the Masjid-i-Suleiman oil field. As a result, Iran has one of the world’s most mature oil sectors. About 80 percent of its reserves were discovered before 1965. Iran has already produced 75 percent of its reserves, so the likelihood of other major discoveries is low. Iran has made some important new discoveries in the past decade, such as the Yadavaran and Azadegan fields, but they have not been sufficient to alter the trend in oil reserves depletion.

Over the years, Washington has imposed escalating waves of sanctions on Tehran, many of which targeted the oil and gas industry. In 2010, it produced some 3.54 million bpd, though by early 2015 production had dropped to around 3 million bpd. In 2011 and 2012, the United States and European Union imposed the harshest round of sanctions to date. By 2014, Iran’s oil exports plummeted from 2.5 million bpd to 1.4 million bpd, their lowest levels since 1986. The limited sanctions relief in the 2013 interim nuclear deal allowed Iran to modestly increase its export of condensates to China and India, but progress quickly leveled off.

Before the sanctions, the National Iranian Oil Company (NIOC) held crude production around 4 million barrels per day range for several years. This was a major achievement since most oil sectors with depletion rates of 75 percent usually witness steep declines in production. Indeed, Iran’s base production is declining around 4 percent per year. The recently discovered new sources allowed Iran to hold oil production relatively steady. They could have even helped production levels to grow somewhat beyond that, if sanctions had not placed other restraints on output.

But new sources may not be able to offset natural declines beyond the short-term. As a result, Iran will have to rely heavily on proven but undeveloped reserves, which will require major new investments. Production capacity is likely to fall because of geological constraints, the lack of domestic technical capacity, financial constraints and international sanctions.

In the 1990s, Iran attempted to attract foreign companies to develop its crude oil reserves, partly because it lacked the technical and financial resources to develop them. The contract terms were called Buy-back arrangements, whereby foreign oil companies developed the field and were paid back in crude oil produced. The field under development was returned to NIOC’s control after repayment was completed. These arrangements were unpopular with foreign companies, even though several large oil and gas fields were developed. Dissatisfaction with the contract, along with the threat of renewed sanctions, led most private Western companies to leave.

The final nuclear deal in 2015 generated renewed interest in Iranian oil, in anticipation of sanctions relief. Iran’s government also issued a new set of contract terms more favorable to foreign companies. Unlike Buy-back contracts, the new Iran Petroleum Contract (IPC) allows companies to participate in all three stages of an oil or gas field’s lifecycle – exploration, development and production.

In a Buy-back contract, foreign companies had a fixed target and were compensated with a pre-determined amount, without the opportunity to increase output through sophisticated means over the field’s lifecycle. The IPC allows for contract changes depending on the complexity of the projects. Other provisions allow foreign companies to participate for up to 25 years – compared to the five to eight years in the original Buy-backs – which increases incentives to maximize production. In 2015, European companies, including Total SA of France, ENI of Italy, Royal Dutch Shell, and British Petroleum (BP), indicated their interest in resuming oil investments in Iran.

Since the end of the 2000s, Tehran has increasingly looked East to attract national oil companies into the Iranian upstream industry. The greatest activity has been with China, which has held talks on major projects since Sinopec signed the contract for the Yadavaran field in 2007. But proceeding to actual development has been slow, even for Yadavaran. The Chinese companies reduced their activities after new U.N. sanctions were imposed. It remains to be seen whether these projects will be reactivated in the near term.

Refining capacity

Iran’s refineries are operated by the National Iranian Oil Refining and Distribution Company (NIORDC). NIORDC operates 15 refineries with a combined crude distillation capacity of 2.04 million barrels per day, according to Facts Global Energy. NIORDC has capacity to produce 1.86 million bpd and has at least nine refineries. Capacity has more than doubled since the early 1990s, and considerable work has been done to upgrade the refineries.

Until recently, Iran primarily refined low-value fuel oil. It relied on imports of higher value-added refined products, such as gasoline, jet fuel and diesel, to accommodate the growing public appetite for subsidized fuels, especially gasoline. NIORDC plans to build five more refineries and three condensate splitters – with the rise in gas production, condensates have become an important source of liquids output. The project could add 2 million bpd to capacity at a cost of $27 billion, according to the Middle East Economic Survey. After sanctions, Iranian officials hope that foreign companies invest in some of this capacity. European and Japanese companies have shown some interest in both investment and construction in the sector.

Natural gas

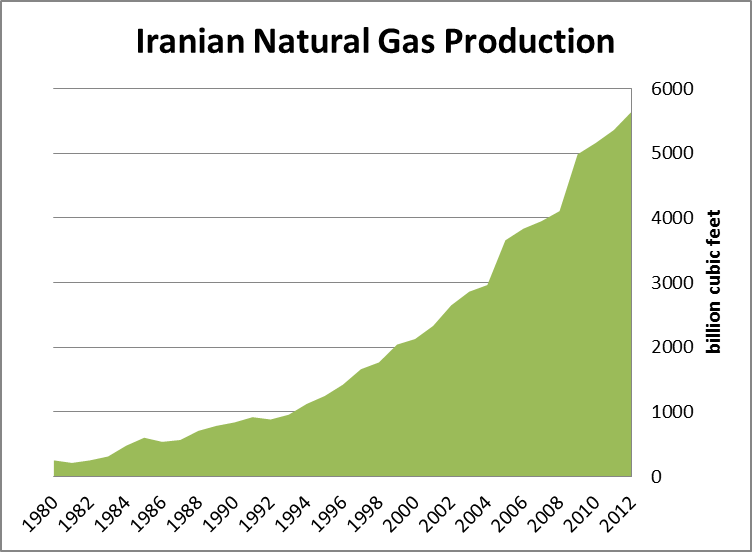

Iran has the second largest gas reserves in the world after the Russian Federation. For two decades, its production growth has increased by an average of 10 percent, yet Iran has only depleted five percent of its gas reserves. Iran’s problem is that its ability to produce has lagged behind its domestic needs. Demand has surged because of economic and population growth. Natural gas has also been liquified and used as a substitute for gasoline and other transport fuels. As Iran's oil sector has become more mature, the government has had to use more gas for reinjection into maturing oil fields in order to maintain oil production.

Iran must continue to develop its reserves at a rapid rate to meet this demand. Iran’s main asset is the giant off-shore South Pars field in the Persian Gulf, which it shares with Qatar. It is the world’s largest gas field. Qatar has sped ahead with development of its field, but Iran has lagged way behind. Tehran has made some progress in developing several phases of the South Pars gas field in recent years. But achieving full potential of this giant field plus other fields will be a challenge over the near term because of technical and financial constraints.

Developing its natural gas sector also requires a heavy commitment to building the necessary infrastructure. Iran’s gas production is in the south of the country, but the bulk of its demand is in the north. It has built an impressive pipeline network to transport this gas, but growing demand has increased the need to expand domestic pipelines.

Since it can barely meet domestic demand, Iran has not been able to deliver on its ambitious gas export program beyond the current pipeline exports to Turkey. Due to sanctions, Iran has not developed the necessary infrastructure to export liquefied natural gas. Regional pipeline projects to Oman and the United Arab Emirates have stalled over pricing disputes. And security concerns have delayed a 2013 plan to build a gas pipeline to Iraq. For its own needs, Iran will continue to rely on gas imports, mainly from Turkmenistan – which are getting more expensive because of competition for this gas from China.

Industry structure and control

The Ministry of Petroleum, which has control over the National Iranian Oil Company, reports to the president with oversight from the parliament. But the dividing line between the ministry and Iran’s oil company is often indistinct. The position of NIOC managing director was only established in 2000 as a separate post. But in reality, as a vestige of the past, the two institutions still share personnel and offices.

The Ministry also controls the National Iranian Gas Company, the National Iranian Petrochemical Company, and the National Iranian Oil Refining and Distribution Company. In 2006, the ministry submitted a bill to parliament proposing that NIOC manage all four companies. But the bill did not pass because Ahmadinejad’s supporters did not want the ministry to create more autonomous companies.

For most of the revolution’s first three decades, an “oil mafia” under the influence of former President Akbar Hashemi Rafsanjani controlled both the ministry of petroleum and the National Iranian Oil Company. Ahmadinejad initially failed to assume control over the sector after his election in 2005. Parliament rejected his first few choices for oil minister. In his second term, he was become more successful in prying control away from the oil mafia, especially after parliament approved Massoud Mir-Kazemi. He has a strong background in the Revolutionary Guards (IRGC) and the defense ministry, which reflects the power shift. He was former head of the IRGC think tank, the Center for Fundamental Studies.

Under Ahmadinejad, the Revolutionary Guards’ influence grew within NIOC, as well as in the service sector. Khatam ul-Anbia, the IRGC construction arm, strengthened its role throughout the Iranian economy, including the oil and gas sector. In 2006, it won a contract to develop South Pars Phases 15-16. In 2009, it took over the Sadra Yard, a firm that has built many platforms in the Persian Gulf and the recently completed Alborz semi-submersible rig which will drill in the Caspian Sea. While the Revolutionary Guards’ profile grew, it also faced financing difficulties. International sanctions have deterred banks from funding Phases 15-16 due to its link with Khatam ul-Anbia.

Under Ahmadinejad, the Revolutionary Guards’ influence grew within NIOC, as well as in the service sector. Khatam ul-Anbia, the IRGC construction arm, strengthened its role throughout the Iranian economy, including the oil and gas sector. In 2006, it won a contract to develop South Pars Phases 15-16. In 2009, it took over the Sadra Yard, a firm that has built many platforms in the Persian Gulf and the recently completed Alborz semi-submersible rig which will drill in the Caspian Sea. While the Revolutionary Guards’ profile grew, it also faced financing difficulties. International sanctions have deterred banks from funding Phases 15-16 due to its link with Khatam ul-Anbia.Starting in 2013, President Rouhani and Oil Minister Zanganeh attempted to alter some of the structural changes undertaken by Ahmadinejad. Zanganeh re-appointed oil ministry managers removed by his predecessor, and has been at least partially successful at scaling back the involvement of the IRGC. He also attempted to slow privatization of oil ministry subsidiaries, though with limited success by 2014.

Trendlines

- The end of international sanctions may revive investment in the oil and gas sector in the short term, which could lead to an increase in oil and gas output.

- The sharply lower oil price could keep the Iranian economy on the defensive, since Iran balances its external accounts around $75 per barrel.

- If sanctions are lifted, higher oil output and exports may increase export earnings. Greater foreign investment in the oil and gas sector may also help boost economic growth and improve the liquidity of external accounts.

Fareed Mohamedi has been an oil and gas analyst for 35 years.

Photo credit: Bijan Zanganeh via Ministry of Petroleum; Ahmadinejad by Daniella Zalcman via Wikimedia Commons [CC BY 2.0]

{kind=link}

This chapter was originally published in 2010, and is updated as of August 2015.

PDF Economy_Mohamedi_Oil and Gas.pdf202.89 KB